Leeward Investment Team

The 2022 midterm elections occurred earlier this week. Here’s how the results impact our thinking about the markets and your portfolios.

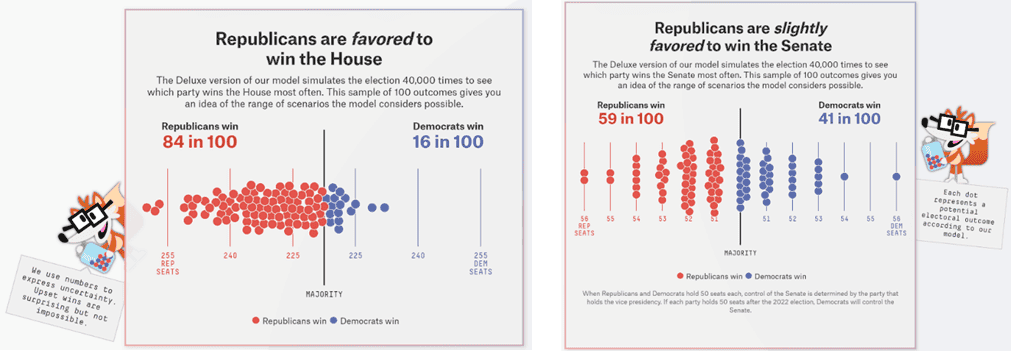

Prior to the elections, we expected Republicans to pick up between 20 to 30 seats in the House of Representatives (House) and gain a majority. At the same time, the Senate looked like a toss-up, with either party only having a slight majority post-election. Our view generally agreed with most polling institutions. Before the election, for example, FiveThirtyEight projected an 84% chance the Republicans would take control of the House of Representatives and a 59% chance they would take control of the Senate.

Source: FiveThirtyEight, as of 11/8/22

Election results mostly were as expected. The House of Representatives will switch to Republican control, and the Senate remains a toss-up. We are surprised that the Senate still remains undecided, but whatever the outcome is, it will be immaterial to markets because the margin of control will be minimal.

Of note, the “red wave” of Republican victories some political commentators had forecast failed to materialize. As we’re writing this, the Republicans have gained seven seats in the House, leaving them the same number of seats short of the 218 seats needed for a majority. The Republicans may get close to 222 seats – enough to take control but not nearly an overwhelming victory. In the Senate, the Democrats managed to flip one seat in Pennsylvania, but Republicans may counter and flip a seat of their own in Nevada. In Arizona, Mark Kelly (D) is expected to win reelection, placing us in a similar situation to 2020, with a December run-off election in Georgia determining whether the Democrats can hold the Senate. If the Democratic incumbent Raphael Warnock wins that race over Herschel Walker (R), the Democrats will retain their majority despite slightly reshuffling the deck furniture.

Over the last two years, there have been two notable legislative bills. The first was the Inflation Reduction Act, and the second was the CHIPS and Science Act. The Inflation Reduction Act of 2022 aims to curb inflation by reducing the deficit, lowering prescription drug prices, and investing in domestic energy production. This legislation is part of President Biden’s policy agenda but was significantly scaled down to get enough votes to pass Congress. The CHIPS and Science Act is designed to boost US competitiveness, innovation, and national security. The law aims to catalyze investments in domestic semiconductor manufacturing capacity. This Act is notable as it is the only legislation passed so far in this Presidential term that has had support from both Republicans and Democrats.

In the future, we expect the President’s policy agenda to narrow. A split congress will make it difficult to pass legislation that is not bipartisan. Activity will focus on infrastructure spending and domestic job creation, similar to the CHIPS and Science Act. These areas are supportive of economic growth and popular with voters.

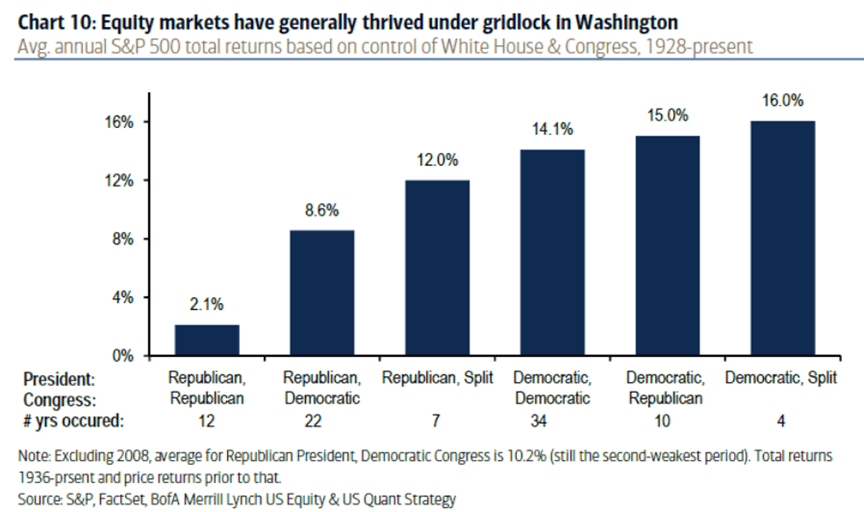

Historically, purple governments have coincided with favorable market environments because split governments tend to have a more challenging time passing sweeping legislation, and markets prefer environments with less political risk.

Since 1928, the most constructive setup for equity markets has been a Democratic President serving with a split Congress (16.0% average S&P 500 return). This scenario is likely for 2023 and 2024. Below is a chart that illustrates market returns under different government make-ups. The most likely scenario today is on the far right.

While the consensus is that the environment we’re moving towards is good for markets, there are a few accompanying risks. Should the economy fall into significant distress (sharp recession) before 2024, it may be challenging to mobilize the government to pass supportive policy. As a result, the market could become even more reliant on the path plotted out by officials at the Federal Reserve. If the Federal Reserve continues to view prices as too high and unemployment as too low, they could tighten policy to the detriment of financial markets. Brinksmanship could also reemerge, particularly around issues such as the debt ceiling, and the potential for government shutdowns popping up in the headlines would rise.

The midterm election results are encouraging for markets. Mixed government control and bipartisan legislative activity are generally good for the economy. Domestic manufacturing will benefit most from the anticipated environment. We focus on high-tech manufacturing, infrastructure building, and capacity expansion as areas of opportunity, which generally fall into the Technology and Industrial sectors in our portfolio allocations. Consumers should also benefit, although it is still too early to say the Consumer Discretionary sector is ready to rebound from its weak performance. We want to see a healthy holiday season for retailers before allocating heavier portfolio weights to this market area.

Most importantly, the risk of midterm elections upsetting the market is now behind us. There were minor surprises but nothing to suggest a significant reassessment of our investment strategies. We are increasingly constructive on markets into 2023.

Thank you for your trust and partnership. Please reach out to us with questions and comments. We look forward to hearing from you.

Sincerely,

Jim and Mike

jim@leewardfp.com

mike@leewardfp.com