Leeward Investment Team

Markets were sluggish to start the second quarter, consolidating their late March gains. Fed Chair Powell ruled out the possibility of a May meeting interest rate cut, pushing bond prices down and commodities higher. By late April, most equity market indices were down 5 to 6 percent as fears of stubborn inflation and a slowing economy sprinkled cold water on the Q1 hot streak. Corporate earnings began to take the spotlight by the end of April, with positive results easing investor concerns. By early May, earnings reports from technology bellwethers MSFT, AAPL, and META pushed large-cap indices to new highs, confirming a continuation of the 2024 rally.

Late in the quarter, a series of weaker inflation and labor market reports provided a supportive backdrop for markets to hit fresh highs, though the advance was driven by a small number of mega-cap technology companies. Volatility picked up in the final weeks of June as investors captured profits going into quarter-end. Overall, investment performance was robust in Q2, and we remain on track for an above-average year.

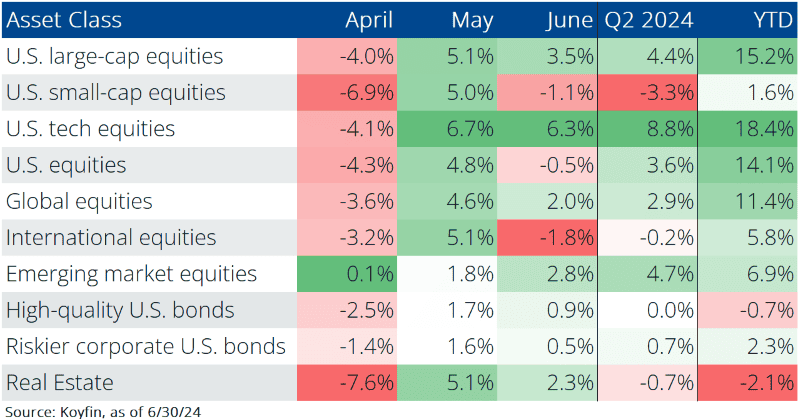

Large-cap U.S. tech companies have remained the place to be invested and outperformed over the quarter. Outside the U.S., international equities fell slightly, driven by Japanese stocks (-3.7%) cooling off after a hot streak in Q1, and French equities (-6.7%) plunging following Prime Minister Macron’s decision to call a snap election the first week of July, which introduced a massive degree of uncertainty around the political future of France. Emerging market equities managed to keep up with U.S. equities this quarter, led by strong performance in China (+8.3%), Taiwan (+11.3%) and India (+10.8%).

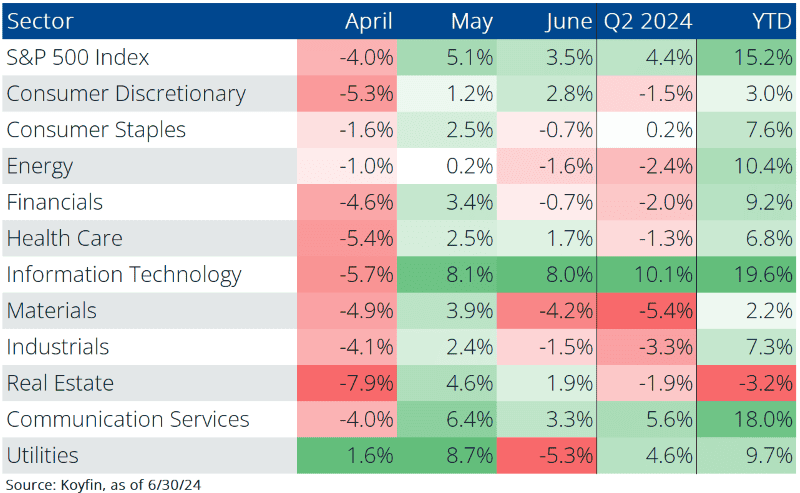

Within the U.S. equity market, only the informational technology (+10.1%), communication services (+5.6%) and utilities (+4.6%) sectors posted significant positive returns, speaking to the lack of breadth in the most recent rally.

In today’s momentum-driven market, holding current winners in portfolios is prudent. However, we are actively monitoring opportunities outside of mega-cap tech companies. For example, data storage, utilities, and infrastructure companies all appear interesting. From a fundamental perspective, the transition toward renewables will require upgrades to existing power grids, increasing electricity rates. At the same time, the ever-growing amount of power necessary to fuel new AI data centers worldwide will substantially increase energy demand. According to the International Energy Agency, the global electricity consumption by AI alone could reach 1,000 terawatt-hours annually by 2026, which is slightly more than the total electricity consumption of Japan. This active monitoring keeps us engaged and ready to seize new opportunities.

Growth is cooling, but forecasters still expect the U.S. economy to increase GDP between 2 and 3% this year. Labor markets remain intact. Unemployment is healthy, at only 4.1% (extremely low by historical standards). Inflation (+3.0%) remains stubborn and is still higher than policymakers and consumers want. Fortunately, price growth hasn’t moved up meaningfully since 2022. Chairman Powell noted “modest further” inflation progress at the June Fed meeting, a shift from his prior statement indicating a “lack of further progress.” Things aren’t perfect, but we’re also not teetering on the brink of recession.

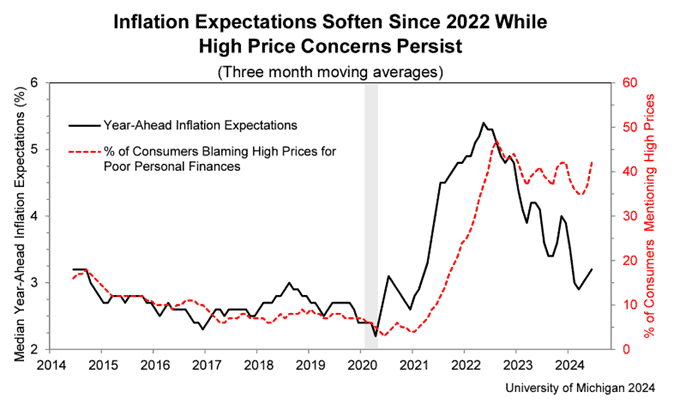

Consumer sentiment is improving but remains 20% below pre-pandemic levels. Concern over high prices is why sentiment has not improved further. Falling inflation will eventually help improve consumer sentiment. For example, although inflation expectations have fallen markedly, the proportion of consumers blaming it for their poor personal finances has not. If history is a guide, the dotted red line in the chart below should turn lower and follow the black line down through the rest of the year, allowing for improved consumer sentiment, which would provide a tailwind for equity market returns.

On the pessimistic side, oil prices have risen above $80 per barrel as we enter the summer driving season. Higher gas prices will likely feed a resurgence in monthly inflation in the summer months, reversing some of the energy impacts in the May report. Additionally, high financing rates for builder and developer loans, alongside ongoing supply-chain challenges, are headwinds for new home construction. Single-family housing starts fell 5.2% in May, equal to production levels seen at the end of 2019.

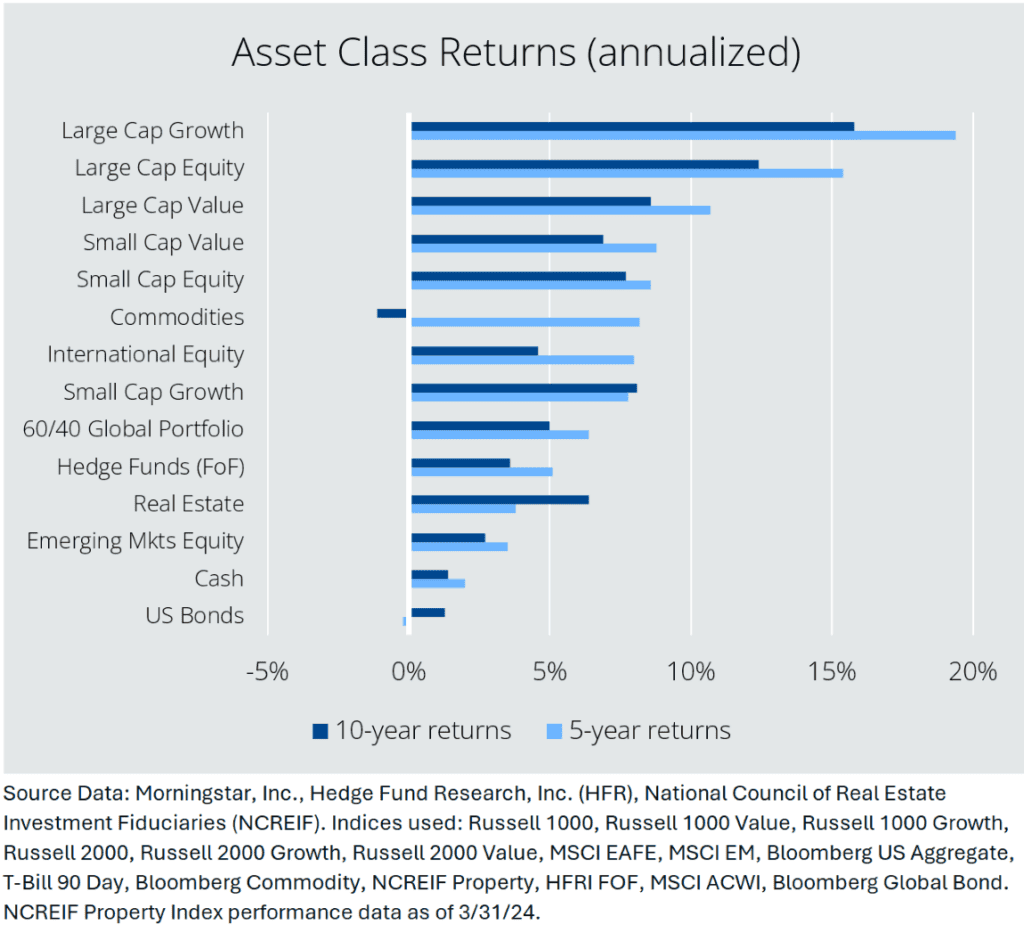

Over the last decade, large, fast-growing U.S. companies have provided the strongest returns for investors. This is our heaviest overweight allocation in client portfolios. Asset allocators refer to this group as “Large Cap Growth” stocks. Since 2014, large-cap growth stocks have returned +15.8% annually. For comparison, small-cap U.S. stocks have grown at about half of that rate (+7.7%), international stocks have returned +4.6%, and emerging market stocks have gained just +2.7%. As seen below, Large Cap Growth (top bars) has significantly outperformed all other asset classes over the last five and ten years, doubling annual returns against most asset classes.

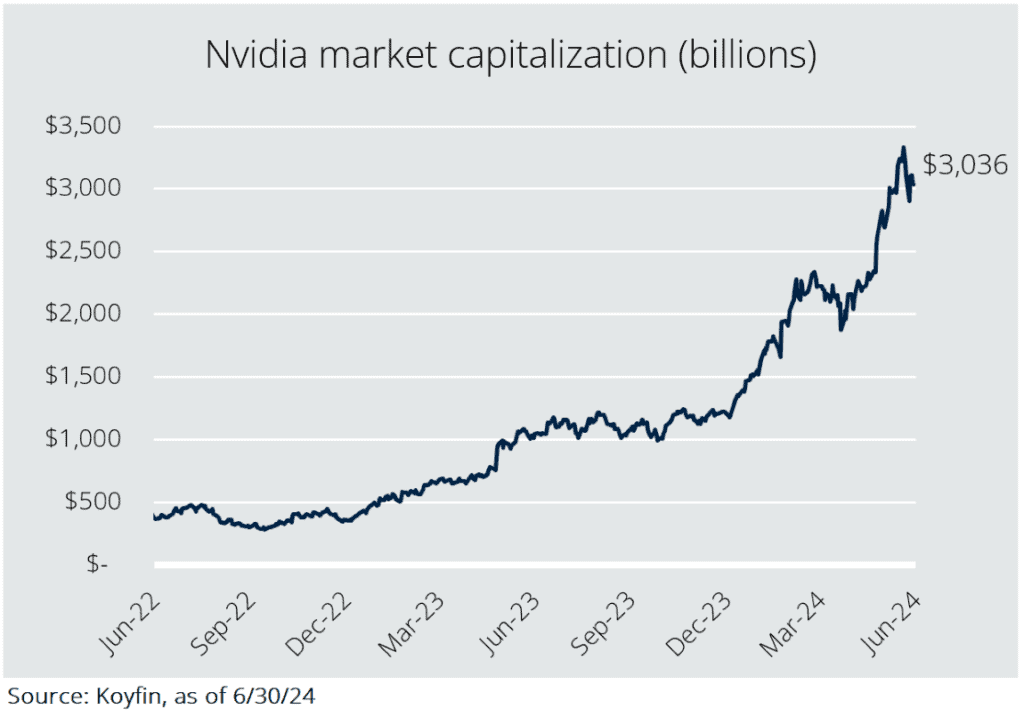

In 2024, the ten-year trend of U.S. outperformance continues. Large-cap growth stocks, led most notably by Nvidia <NVDA>, marched higher in the second quarter. Some skeptics voice concern over the outsized impact of a small group of high-flying companies. For example, Nvidia's market capitalization grew by $1.9 trillion to $3.1 trillion in the first half of 2024. For context, the entire German stock market has a market cap of about $2.2 trillion.

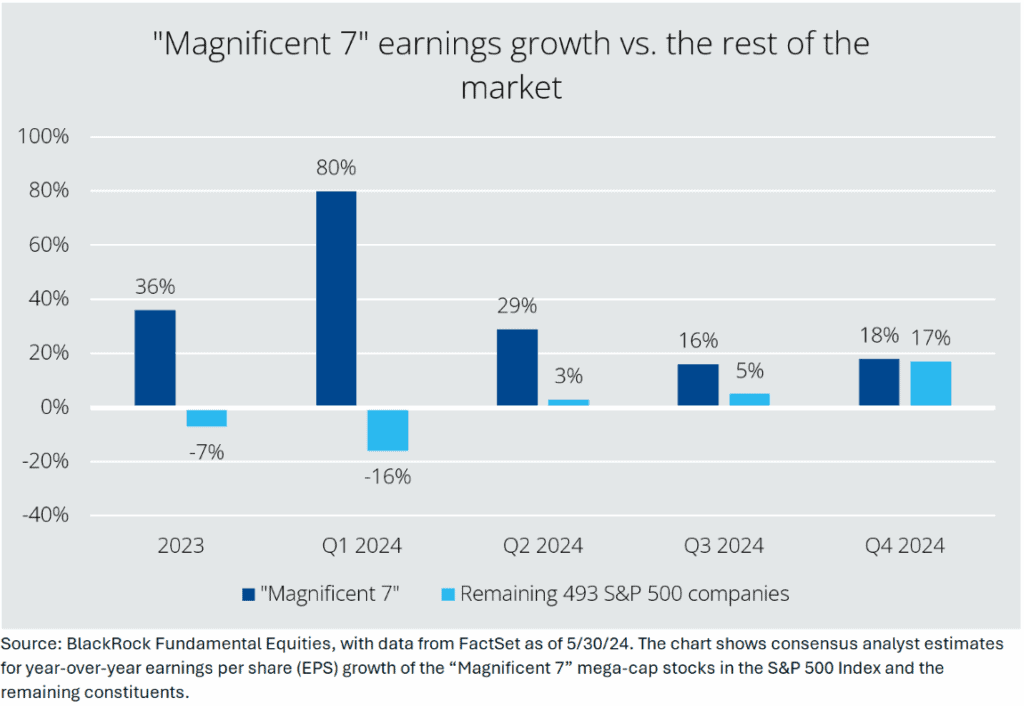

We believe the answer is yes; relative outperformance will continue. One of the biggest reasons is the strong earnings growth of large-cap growth stocks compared to the broader market. For example, the “Magnificent 7” (meaning Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla) earnings grew 80% last quarter (see chart below), while the rest of the S&P 500 index earnings shrank by -16%. We expect a similar trend this earnings season. By year-end, however, the gap is expected to become almost negligible. By 2025, “Mag 7” earnings growth is expected to be in line with the rest of the index. As earnings growth balances across the index, the market will broaden beyond its current leaders, enabling new U.S. companies to outperform. We anticipate the resulting environment will be rife with opportunities, and we will adjust portfolios to focus on new areas of earnings growth.

While the U.S. consumer continues to drive solid economic growth, we are seeing signs of consumer fatigue. Credit card delinquencies are rising and are now greater than pre-pandemic levels.

In the labor market, we are reaching an inflection point. The job vacancy rate has fallen to 5% from pandemic-era highs of 7-8%. If the job vacancy rate falls much further (in other words, demand for labor falls much more), the unemployment rate will accelerate higher. Any marked increase in the unemployment rate will be viewed negatively for the economy and change the conversation around the number of interest rate cuts on the menu for early next year.

The equity market has exhibited narrow leadership (only a few stocks account for most of the market’s gains), but that tends to be the case in most cycles. Valuations are steep in some areas but not frothy. Earnings growth has been impressive, as have the positive earnings revisions, and we believe earnings growth outside of the Magnificent 7 can improve through the end of the year.

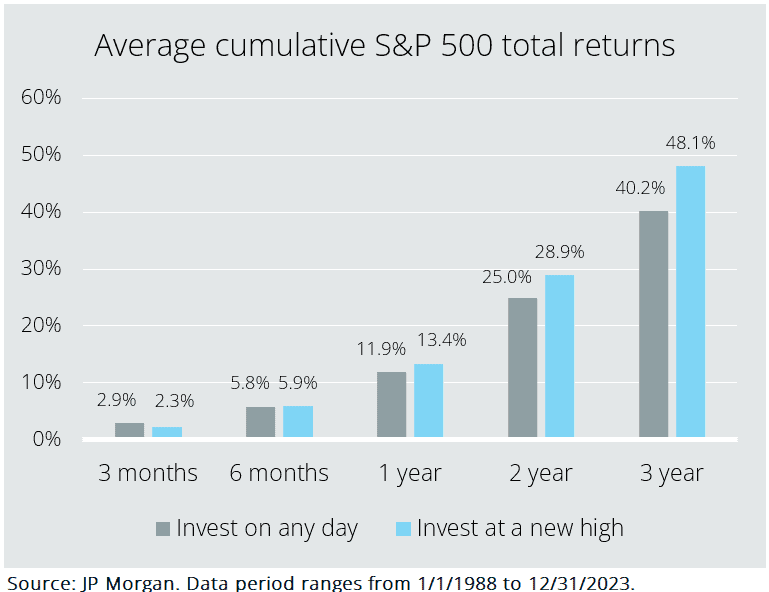

It is normal to feel uncomfortable buying stocks near all-time highs, but as the chart below shows, it has actually been a good strategy to do just that over the past 35 years. In almost all cases, investing at market highs has led to higher returns over the next 1, 2, and 3 years.

The trends that drove markets in the first quarter – strong corporate earnings, stubborn inflation, and weak bond performance – continued throughout Q2. In client portfolios, we avoided heavy profit-taking but did look to adjust positions and improve overall quality. We slightly increased industrial exposure to take advantage of positive infrastructure spending trends. We shifted exposure within both healthcare and consumer sectors to find better-performing companies but retained underweight positions in both areas. We continue to maintain our large-cap growth bias in equities and U.S. companies.

For clients with fixed-income allocations, we have largely held existing positions. Bond performance has been disappointing so far this year, but we believe the asset class is positioned to do well in the future. We’ve resisted becoming more aggressive in this area for now, instead relying more broadly on equity performance to drive overall portfolio growth.

We remain optimistic about the market and believe investors are best served fighting the urge to de-risk portfolios. Inflation is in check, and monetary policy is muted. The consumer is weakening as stimulus checks move farther into the rear-view mirror, but slowing price increases should help improve sentiment and keep a ceiling on interest rates. Corporate America remains healthy and we expect to hear positive commentary from management teams in July. If that is the case, markets should continue to grind higher, and our goal is to capture as much of that upside as is prudent. Many stocks have been left behind in the rally over the last year and are now trading at attractive valuations. We will be watching these opportunities closely and aiming to capitalize where possible. We’ll continue to monitor election scenarios, but at present, uncertainty is high, and analysis is less useful. We will have much more to say after the Democratic National Convention in late August and in our Q3 commentary in early October.

We appreciate your business and partnership.

Best,

Jim and Mike

jim@leewardfp.com

mike@leewardfp.com