Leeward Investment Team

Markets experienced a pullback in the first quarter, with U.S. equities declining as much as 9% from their February highs, though they ended the quarter down just -4.4%. The turbulence has been driven by the escalation of the conflict involving the United States, Israel, and Iran, particularly Iran’s efforts to disrupt energy flows through the Persian Gulf.

Since late February, tensions have centered on the Strait of Hormuz, a critical shipping route for global oil supply. Threats to commercial shipping and intermittent disruptions to tanker traffic have constrained flows and introduced a meaningful supply shock to energy markets. In response, the United States has taken steps to secure the region while continuing to signal openness to a negotiated resolution.

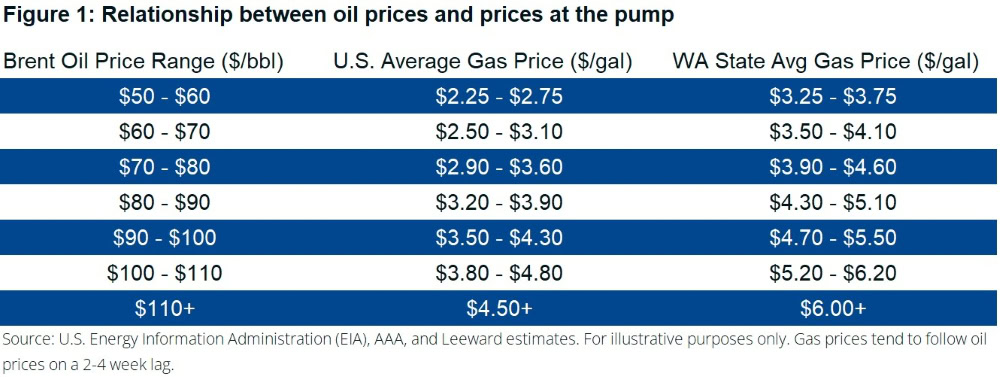

This has translated directly into higher energy prices. Brent crude has moved above $100 per barrel, and U.S. gasoline prices have risen above $4 per gallon, representing the most significant energy-driven inflation risk since 2022. Figure 1 below shows how oil prices have generally flowed through to gas prices both nationwide, and within Washington state specifically.

In comments last night, President Donald Trump indicated that while the conflict may be “nearing completion,” key objectives have not yet been achieved and offered limited clarity on a path toward de-escalation. He left the future status of the Strait of Hormuz unresolved and signaled that U.S. allies may play a larger role in maintaining energy flows, while emphasizing that the United States is less directly dependent on those supplies.

Taken together, the tone suggests continued near-term pressure before a more durable resolution emerges. This points to an environment characterized by elevated energy prices, renewed inflation pressure, and increased volatility across both equity and fixed income markets. While geopolitical developments will drive near-term movements, they do not materially alter our broader investment framework.

Markets responded modestly. Equity futures declined approximately 1% following the speech, while Brent crude moved higher from roughly $100 to $105 per barrel.

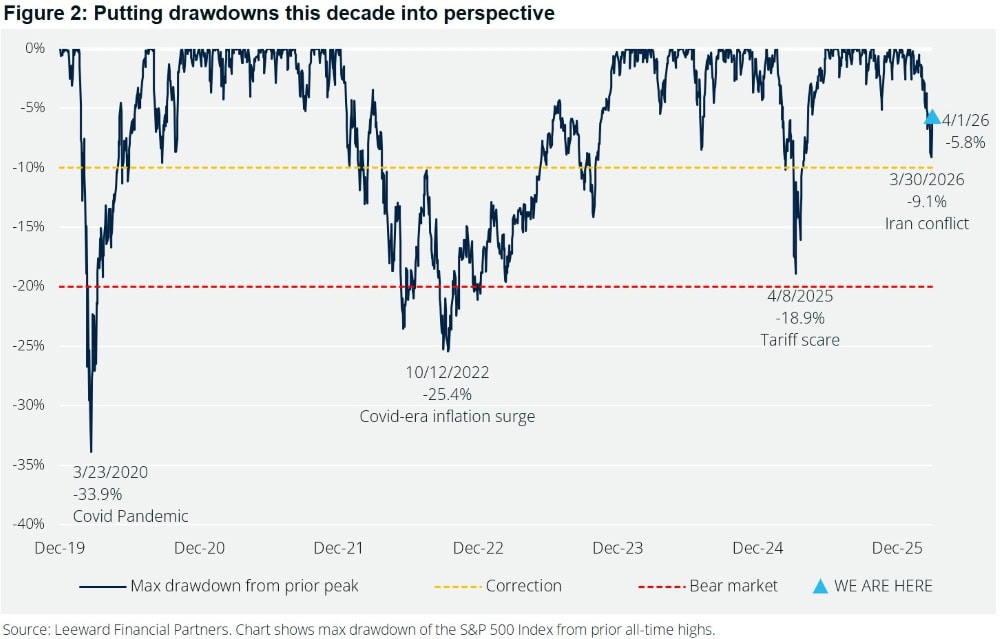

Against this backdrop, the overall market reaction has remained relatively contained. While equities briefly approached correction territory, markets have already recovered a portion of those losses. The S&P 500 declined 4.4% in the first quarter of 2026 and, as of yesterday’s close, remains less than 6% below its all-time highs.

Pullbacks of this magnitude are a normal and healthy feature of equity markets, even during strong multi-year advances. While day-to-day volatility has increased, the broader backdrop remains constructive, and portfolios are holding up better than in prior drawdown periods this decade (see Figure 2 below).

The conflict has now been ongoing for approximately four weeks, broadly in line with initial expectations. Iran’s use of irregular tactics has raised the cost of further escalation and slowed progress toward U.S. and Israeli objectives, particularly through continued pressure on energy flows in the Strait of Hormuz.

In light of recent comments from President Donald Trump suggesting limited near-term de-escalation, we believe the administration is pursuing a path that balances continued pressure with an eventual off-ramp to reopen the Strait. Under this framework, we see three potential paths forward:

1. Rapid de-escalation

The U.S. and its allies step away relatively quickly, allowing the Iranian regime to remain in place while shifting toward non-military pressure. Energy flows normalize, oil prices decline, and risk assets recover.

We view this as possible, but less likely.

2. Gradual de-escalation (Base Case)

The conflict persists for weeks or months before stabilizing. Energy prices remain elevated, inflation pressure builds, and equity markets remain range-bound. Corporate earnings hold up, but consumers feel the impact through higher gasoline and energy costs.

We view this as the most likely path forward.

3. Further escalation

The U.S. intensifies efforts to secure the Strait, prolonging disruptions to global energy flows. This would likely result in higher inflation, weaker growth, and sustained pressure on equities.

We view this as plausible, but least likely.

Under our base case of gradual de-escalation, the primary economic impact is driven by the persistence of elevated energy prices rather than the magnitude of the initial shock. What was initially expected to resolve in a matter of three to five weeks now appears more likely to unfold over several months, extending the period of pressure on energy markets.

While oil prices have recently moved above $100 per barrel, we expect moderation over time toward the $85–$90 range. This remains well above pre-conflict levels but below the threshold that typically causes lasting economic damage, resulting in sustained but manageable inflation pressure.

Emerging market economies, particularly energy-importing countries such as India, Vietnam, and Turkey, face the greatest pressure. Higher oil prices widen trade deficits, weaken local currencies, and increase the cost of USD-denominated energy imports. This dynamic feeds through to higher inflation and, in some cases, tighter monetary policy, weighing on growth.

Developed economies outside the U.S., including much of Western Europe and Japan, also face a headwind. As net energy importers with slower growth and limited domestic production, they are less able to offset higher prices. In these economies, energy costs act as a direct tax on consumers and industry, compressing margins and weighing on demand.

By contrast, net energy exporters are better positioned. Countries such as Brazil and Mexico, along with parts of the Middle East, benefit from improved terms of trade and stronger near-term growth.

The United States sits between these extremes. As a major energy producer and net exporter, higher prices support domestic production, investment, and export revenues. At the same time, elevated gasoline and energy costs weigh on consumers and discretionary spending. At current levels, these forces largely offset, leaving the U.S. relatively well insulated compared to other developed economies. The balance becomes more challenging if prices move sustainably above $100 per barrel, where consumer and inflation pressures have historically outweighed the benefits to the energy sector.

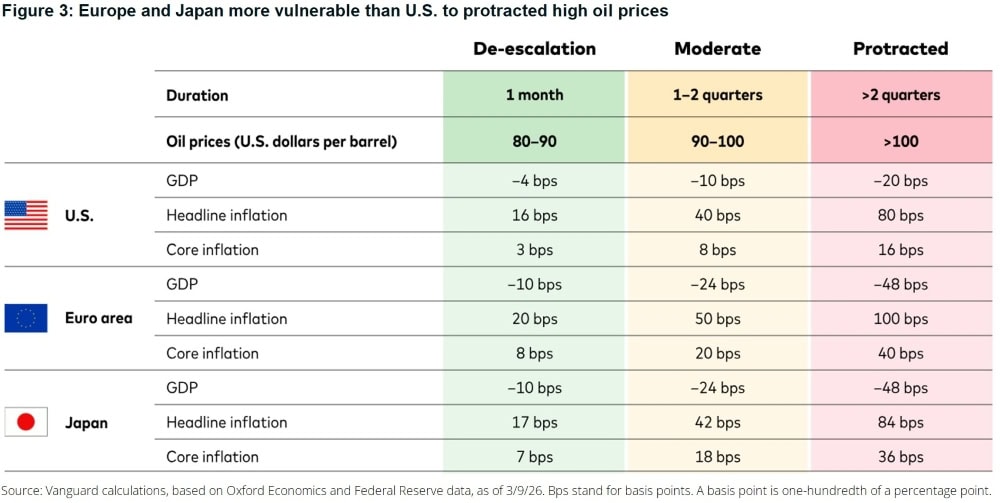

Figure 3 below shows that higher oil prices impact everyone, but hurt Asian and European economies much more than the U.S.

Sustained, but not extreme, energy prices are likely to keep headline inflation elevated while having a more limited impact on core inflation. This dynamic leaves policymakers in a holding pattern, balancing persistent inflation pressures against a gradually slowing economy.

At the start of the year, markets were expecting one to two rate cuts in 2026. That outlook has shifted meaningfully. We now see a higher likelihood of no changes this year, or at most a single cut later in the year, as the Fed remains cautious in the face of elevated energy-driven inflation.

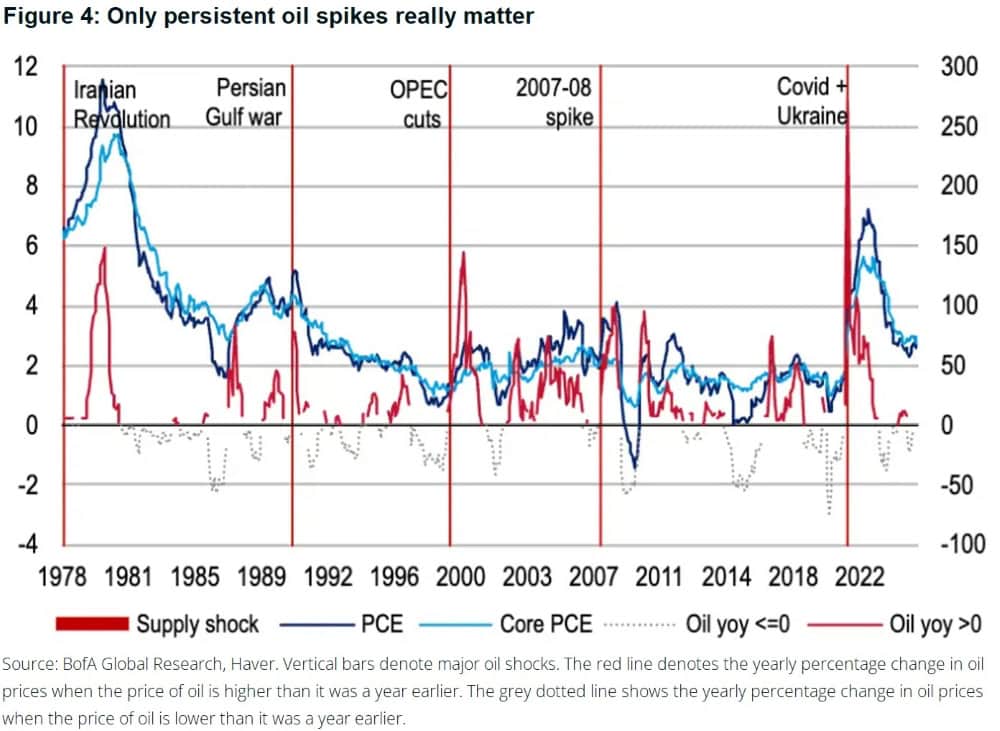

Importantly, short-term spikes in oil prices are less consequential than the persistence of elevated levels. Inflation tends to respond more meaningfully when higher energy costs are sustained over time, rather than during brief dislocations (see figure 4 below).

As noted by Vanguard’s senior U.S. economist Josh Hirt, “energy-driven supply shocks are not something that monetary policy is designed to address.” In practice, the Fed tends to look through temporary energy-driven inflation, responding more forcefully only if higher prices begin to feed into broader, more sustained trends. In other words, higher oil prices alone are unlikely to prompt rate hikes, but they can delay the timing of policy easing.

There are, however, offsetting forces. Disinflationary pressures tied to productivity gains from AI, along with the rollback of certain tariffs, should help ease price pressures over time and support the eventual resumption of rate cuts.

Provided oil prices remain below the more disruptive levels discussed earlier, we view the current environment as one where volatility is creating opportunity rather than signaling a need to become more defensive. Periods like this tend to reward patience and discipline over reactive repositioning.

In early March, we made targeted adjustments to client portfolios in response to evolving dynamics around AI and a shifting global backdrop. We modestly increased international exposure, funded through reductions in real estate and some profit-taking in large technology companies. We have retained an overweight to semiconductor companies and remain underweight software, where the timing and magnitude of AI-driven returns remain uncertain.

Recent weakness in the software sector has contributed disproportionately to market declines, particularly given its leadership in recent years. While we expect clear winners and losers to emerge as AI adoption evolves, we believe a combination of energy-related uncertainty, weaker sentiment, and technical pressures has driven a compression in valuations across many high-quality companies that continue to deliver strong earnings.

Across sectors, we have increased exposure to Healthcare and refined our positioning within Financials to improve industry exposure. We’ve taken some profits in consumer staples in more conservative accounts, where valuations had become less compelling.

In fixed income, our positioning reflects a more cautious view on inflation and interest rates. Earlier in the quarter, we increased exposure to longer-term bonds. We have since begun to reduce that exposure as the risk of more persistent inflation has increased. Instead, we are emphasizing higher-yielding bonds, which are less sensitive to changes in interest rates in the current environment. Overall, we remain conservative in our bond allocations. We may increase exposure to longer-term bonds if inflation concerns begin to ease, but we are not at that point yet.

The recent market pullback is creating opportunities. The S&P 500 is down less than 6% as of this writing. This is despite war, an oil spike, elevated interest rates, continued anxiety around AI disrupting nearly every industry, and large technology companies having moved sideways or lower for the better part of six months.

A key reason for this relatively modest drawdown is that we entered the year with strong underlying fundamentals. U.S. earnings growth remains solid, fiscal support has been favorable, and we are beginning to see an increase in tax refunds flowing back to both consumers and businesses. At the same time, valuations have reset, with many high-quality companies now trading at more attractive levels.

As we move through the year, we expect investors to refocus on core drivers and business fundamentals, supporting a more constructive backdrop for equities. We are actively building our list of opportunities. Several sectors, including Technology, Communication Services, Financials, and Industrials, are now in or near correction territory. Within these areas, semiconductor companies, money center banks, and transportation and logistics businesses stand out as particularly compelling at current levels. We are also intrigued by software companies, but are not yet willing to commit significant capital as visibility around returns on AI investment continues to evolve. More broadly, we believe Financials and Technology are well positioned, as valuations have reset while underlying growth profiles remain intact.

We’ve seen environments like this before. Periods of uncertainty and volatility often create the best opportunities, particularly when underlying fundamentals remain intact. Our focus remains on staying disciplined, taking advantage of dislocations where they appear, and positioning portfolios for the opportunities that emerge on the other side of this cycle.

Thank you for your trust and partnership, and please reach out to us with any questions you may have regarding your portfolio.

Best,

Leeward Financial Partners